🧨 Your index fund has never met this Fed Chair. Today it does

Half of former Fed officials expect a hike — gold at $4,354 and the dot plot decide today...

WEDNESDAY MARKET UPDATE

Today is the day. Warsh speaks at 2:30. The dot plot drops at 2:00. Half of the former Fed officials surveyed think he'll have to raise rates this year. The market thinks he won't. Someone's wrong.

🟩 | Retail sales surged 0.9% in May — nearly double the 0.5% consensus; the consumer refuses to slow down.

🟩 | Dow hit a record above 52,000 Tuesday — then the Nasdaq gave back 1.15% on tech profit-taking.

🟥 | Oil at $76 WTI — below $80 for the first time since March 4; down 34% from the $115 peak.

Gold & Macro

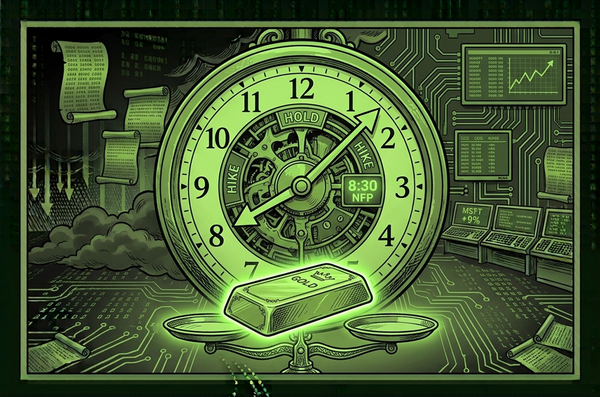

GOLD WAITS. THE DOT PLOT DECIDES

Gold at $4,354 this morning. Flat. Frozen. The same oil-crash-to-gold-rally thesis I described Monday is still intact — but nobody is trading it. Everyone is waiting for 2 p.m.

Here's the paradox Warsh faces. Retail sales just printed +0.9% — nearly double consensus. That's not a consumer that needs help. But oil is at $76, down 34% in three weeks. June CPI should fall hard from May's 4.2%. He has strong spending data arguing for hikes and collapsing energy costs arguing for patience. A Duke survey found half of 34 former Fed officials think he'll have to raise rates this year. The dot plot at 2 p.m. tells us where his committee stands.

If the dots show no hikes and Warsh signals patience, gold rallies toward $4,500. If three members project hikes — as Goldman expects — and Warsh sounds hawkish, gold retests $4,200. Silver at $71.24 moves with it. The rate-hike odds have already pulled back from 70% to 57% since the deal. That's a tailwind — unless Warsh reverses it at 2:30. In an environment this uncertain, plenty of institutional capital is finding its way into hard assets and early-stage innovation.

The Trade

THE CONSUMER SPENT 0.9%. THE FED NOTICED

The Nasdaq dropped 1.15% Tuesday. Nvidia fell 2.4%. Broadcom lost 4.4%. Micron sank 6.2%. AMD cratered 7.3%. Intel gave back 8.5%. That wasn't a selloff — it was profit-taking after Monday's 3.1% Nasdaq surge. But the Dow hit a record near 52,000. Two different markets in the same session.

The bigger story is the consumer. May retail sales at +0.9% — with $4/gallon gas and 4.2% CPI — is the number that complicates everything. The market wants Warsh to be dovish. The data doesn't support it. A consumer spending this aggressively doesn't need rate cuts. And housing starts just dropped 15.4% — the weakest since May 2020. Hot spending, cold housing, crashing oil. This isn't a simple economy. It's three economies stacked on top of each other.

Meanwhile Trump said the deal is “not yet final” and the U.S. will “go right back to dropping bombs” if needed. Oil at $76 heard that and didn't flinch. The market is calling his bluff.

What to watch:

2:00 p.m.: FOMC decision + dot plot + economic projections. 2:30 p.m.: Warsh's first press conference. Thursday: jobless claims, Kroger, Lennar, FedEx earnings. Friday: Iran deal signing in Switzerland — markets closed for Juneteenth.

Heat Check

Nathan’s Take

“Half of former Fed officials think Warsh hikes this year. The market is pricing zero. Somebody's portfolio is about to get a lesson at 2:30”

Names to Know

SPACEX, NVIDIA, INTEL

SpaceX $SPCX ( ▼ 3.51% ) — rose again Tuesday, now above $169; market cap briefly passed Microsoft; acquiring Cursor AI in a $60B deal.

Nvidia $NVDA ( ▼ 0.08% ) — led Tuesday's tech profit-taking after Monday's 3.1% Nasdaq surge; AMD fell 7.3%, Intel sank 8.5%.

Intel $INTC ( ▲ 3.07% ) — bouncing Wednesday after announcing new chip partnerships; the AI-driven renaissance under CEO Tan continues.

Amkor Technology $AMKR ( ▲ 4.3% ) — semiconductor packaging company jumped after signing a 10-year manufacturing deal with TSMC.

BMW $BMWYY ( 0.0% ) — cut 2026 profit outlook, citing weakening China demand and Iran war disruptions.

For real-time data, I recommend monitoring Finviz.

The Macro Edge

🏠 | Housing starts collapsed 15.4% in May to 1.177 million — the lowest pace since May 2020.

💣 | Trump warned the deal is “not yet final” and the U.S. will “go right back to dropping bombs” if needed — oil didn't move.

🚀 | SpaceX acquiring Cursor AI in a $60 billion deal — the AI coding startup becomes part of Musk's empire.

🇯🇵 | Bank of Japan raised rates by 25 basis points to 1% — global tightening continues even as the deal eases oil.

⛽ | U.S. gasoline dropped below $4/gallon for the first time since April — oil's 34% crash is finally reaching the pump.

Two o'clock changes everything. Or nothing. Either way, you'll know by 3.

Nathan Reed | Profits & Insights